Thesis

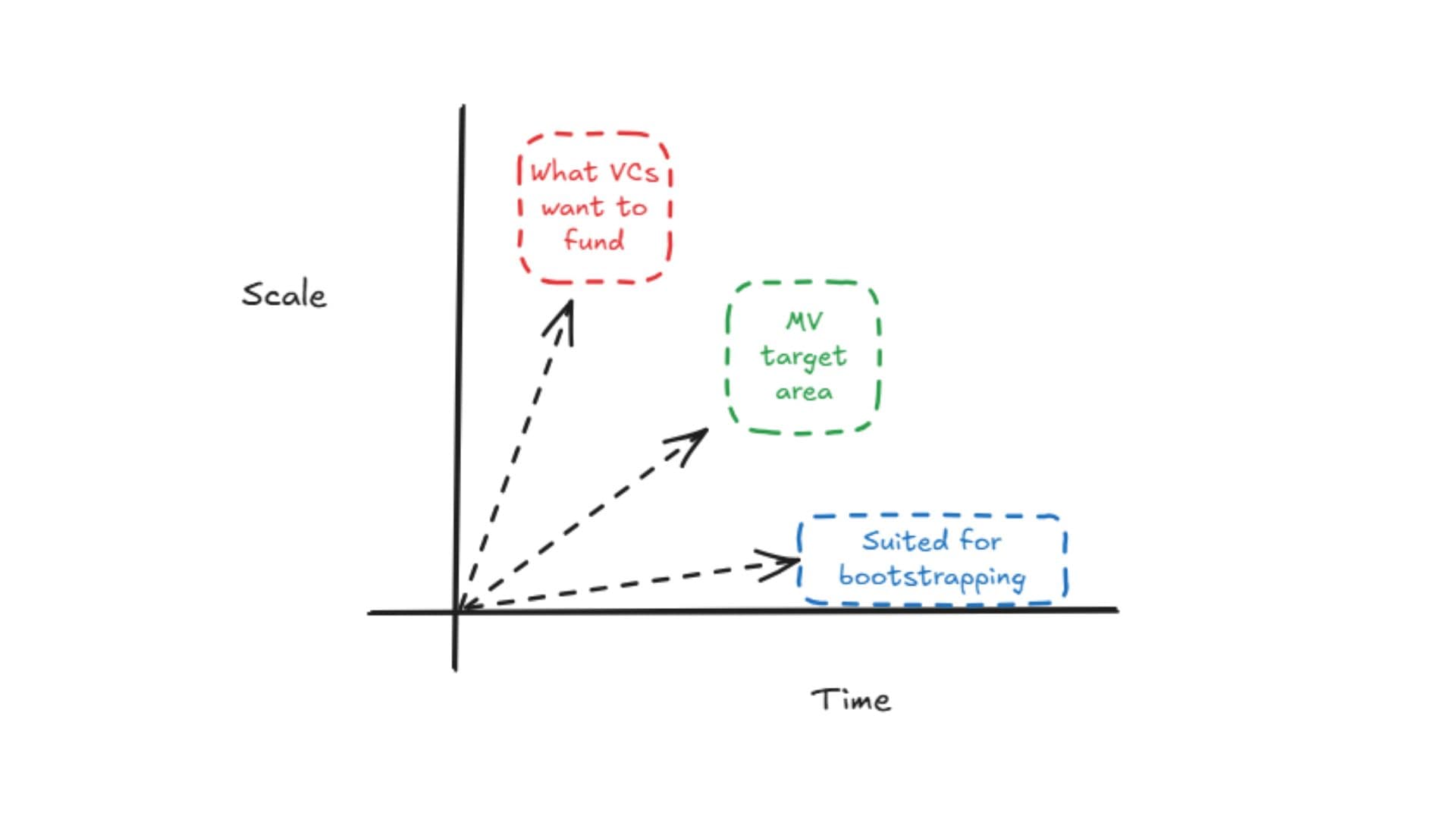

Malpani Ventures is a sector-agnostic investment firm funding frugal innovation in India. We back founders with patient capital, because building a real business takes time. We focus on cash flow and customers, not flashy hype.

What we look for

Signals that show a company is already working and ready to scale with discipline.

- Paying customers. We invest in companies that already have real users or revenue - our checks are for growing what works, not building prototypes.

- Small, smart rounds. Ideally you have raised a tiny round (INR 1-3 Cr) and are growing sensibly. Show us the numbers: revenue, retention, and margins.

- Built to last. We want to back founders who run their company like a business, not a startup. Focus on profit and sustainability, not fads or frenzy.

- Solid team. Founders who hustle and complement each other - creative, frugal operators.

- Clear, no-nonsense plan. A straightforward roadmap to break-even - no buzzwords or hidden agendas.

Resources

Templates, checklists, and explainers we share with founders.

Thesis Q&A

- A large addressable market.

- A wide moat created by using tech or a unique product or service as a critical component, with product development largely done and a strong business model.

- Companies gaining traction (current traction of at least Rs 5-7 lacs) by using their finances frugally.

- At least two co-founders with prior startup or domain experience who complement each other with a diverse skill set.

- Businesses where the unique model can assist founders to leapfrog competition irrespective of deep pockets in the ecosystem.

- We like to operate in the angel stage where valuation and fundraising is in our comfort zone.

A compelling insight into the industry you operate in. We like to see what our founders understand about the market or a need that others do not.

We prefer companies with traction of at least Rs 5-7 lacs MRR because early customers are the biggest validators of a business idea.

We prefer founders to get their funding from their customers (i.e. revenues) because that is the strongest credible source of information that we, as outsiders, can analyze.

We like companies with strong margins that help solidify their value proposition over time.

We also prefer finances being used frugally to squeeze every penny for sustainable growth. Creative thinking and meaningful go-to-market strategies matter because focus works.

No. We invest in companies across India.

While we will definitely have some concentration in Mumbai and Bangalore, we are interested in companies across the country.

We have a soft corner for founders from tier 2 and 3 towns.

No. We do not have any strict ownership requirement.

However, we like to have enough stake in the company to make sure we can be meaningful participants given our time and resources.

No round is too small for us. The average size of the round we participate in is approximately Rs 2-8 cr.

We also invest in rounds as small as Rs 50 lacs and as large as Rs 10 cr.

Startups are fragile organizations whose valuation cannot be determined by traditional cash flow models. Hence there is no science behind the true valuation of a startup.

Given our ticket size and ownership requirements, we like to participate in startups with pre-money valuation anywhere between Rs 15-35 cr.

However, we have also invested in companies above and below our sweet spot. Your value proposition has to be significantly strong for commanding a higher valuation.

While we are happy leading a round, we are not the lead investors half the time we invest.

We have a track record of partnering with experienced seed and angel investors and funds. For us, having our interests aligned and protected, and having a meaningful stake is paramount.

We have found that it is in the best interest of startups to have an active lead investor.

Lead or no lead, we are ready to support our startups.

No. We would explain, but we find Brad Feld explains it better.

No. We do not take board seats.

But we request that founders grant us board observer status, freeing up the board for founders, institutional VCs, and independent members.

We prefer companies to have their affairs in order before we enter. Some of the standard conditions precedent that we require are:

- Formal incorporation of the company and any of its allied businesses in a single entity (or its subsidiaries if being run under personal names).

- ESOP pool set up prior to funding.

- A 36-month KMP and founding team compensation plan.

- All intellectual property, websites, domain names, and technology transferred in the name of the company.

- Agreement on format and period of monthly information reports to be shared with us.

- Alignment on broad direction, including a one-pager of achievements and key operating metrics, key priorities for funding and plan for reaching operating breakeven, and monthly progress review calls with MIS shared prior to the call.